End of Year Tax Planning

Well, we are approaching the end of another year. So, while many of us are running around with our hair on fire, it’s not likely that we are stopping to consider how we can improve our tax situation, but this can be done too.

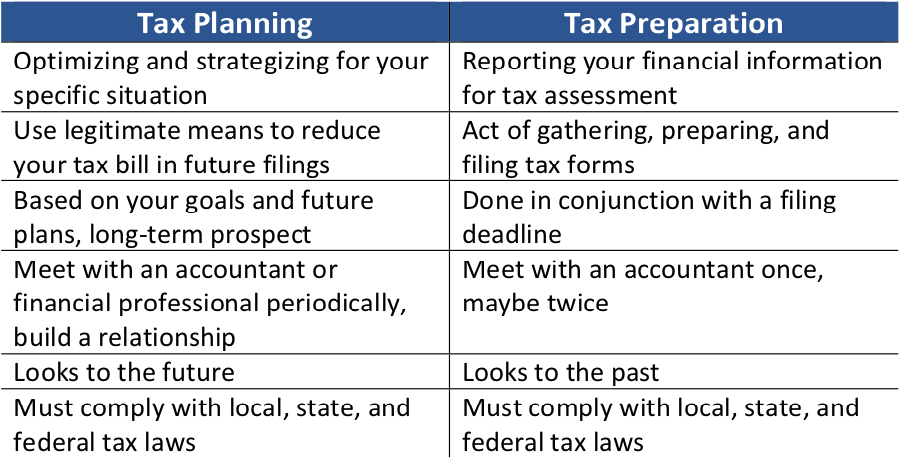

What I’m talking about is tax planning, not just tax preparation. There are some differences between these as outlined below.

So, what this means is that while we are required to accurately report, there are actions that can be taken in many situations to improve how much we need to pay in taxes. Additionally, actions we take today can have a significant affect on our future tax bill and are well worth the effort.

What’s in the new law?

You may be aware that some new tax laws went into effect for tax year 2018 with the signing of the Tax Cuts and Jobs Act in 2017. How will it affect you? Let’s take a look at some of the big changes.

Paycheck Withholdings

Some may have noticed changes in their income withholding since the formula for automatic withdrawal changed. How do you know how much to have withheld from your income? Check out the IRS’s Withholding Calculator HERE (or copy this link into your browser: https://www.irs.gov/individuals/irs-withholding-calculator?mod=article_inline). Keep in mind that if you are getting a big refund, you are in effect giving Uncle Sam an interest free loan!

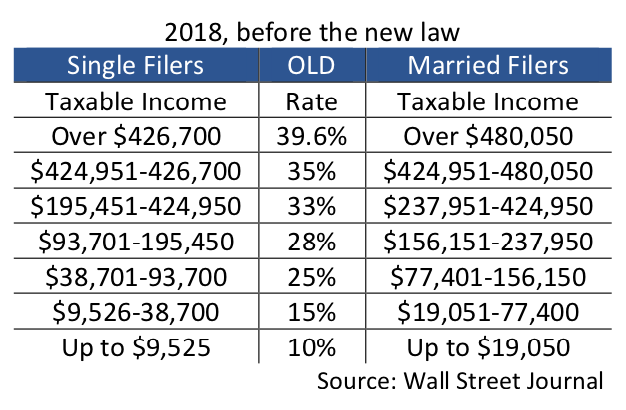

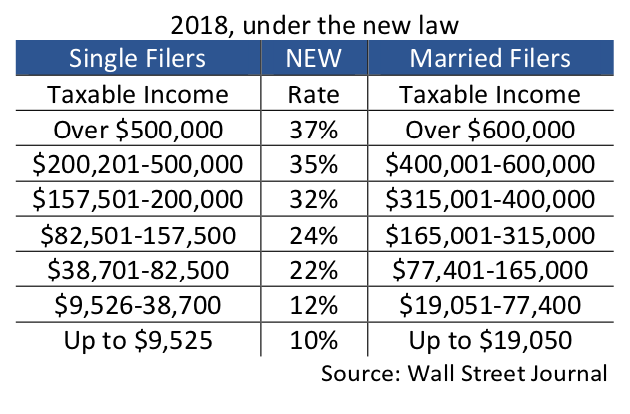

Updated Tax Brackets

2018 income tax rates are actually friendly to most filers. Take a look at the charts below for comparison.

Personal Exemptions

Personal exemptions have been suspended through 2025. This could add up to about $4,000 per family member prior to the new law, but it is no longer available.

Alternative Minimum Tax

If you had to pay the alternative minimum tax (AMT) in previous years, now you may not. The new law is expected to reduce the number of these filers required to pay AMT from 5 million to about 200,000.

State and Local Taxes

State and local tax deductions have been reduced to $10,000 for joint filers and $5,000 for single filers. Higher-taxed filers will inevitably notice this more than their lower-taxed counterparts.

Mortgage Interest Deductions

The mortgage interest rate for mortgages used for primary home purchases has also been reduced for 2018 from mortgage balances of $1 million to balances $750,000. It’s important to note this new lower limit applies only to homes purchased after December 17, 2017. Existing loans before then up to a million dollars can still deduct their interest.

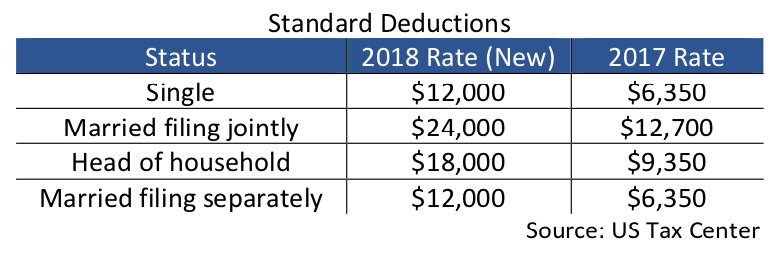

Standard Deductions

Many write-offs were also suspended or reduced. This means that for many filers who found it advantageous to itemize your deductions, it may no longer be the case. The new standard deductions did increase, so that’s good news.

Giving to Charity

If you’ve accounted for charitable contributions in the past, you still can, but you may want to strategize. Because the threshold for itemized deductions has increased, it may be more advantageous to lump multiple years’ donations into a single year. One way to do this is through a donor advised fund.

What about the kids?

The child tax credit increases from $1,000 to $2,000 and couples making up to $400,000 can now qualify for the full amount ($200,000 for single filers) and it phases out for those with higher incomes. However, once your child turns 17, it no longer applies.

If you have a 529 Plan for your child, there aren’t any big changes with regard to your taxes, but there are some changes in how you can use it. Now, you can use up to $10,000 per year, per child for K-12 tuition and secondary education. Not all states are on board with this, but Washington is. This is in addition to other expenses, such as room and board, computers, books, and other qualifying expenses.

For children who have income, the new law no longer ties your child’s tax rates to your own. Instead, the rates are based on the income source, how much it is, and your child’s age.

Small Business and Corporate Tax Changes

This is one area where it may be best to confer with a specialist, but here are some considerations to get you started.

Depending on your situation, you may find it advantageous to defer income. Instead of including it in 2018, accounting for it in 2019 may reduce your overall tax liability. Figuring out whether to defer or not is a process where planning should include several years if you want to get the most out of it.

If you buy new equipment or wish to account for depreciation, it must be “placed in service” by December 31st of that tax year.

Owners’ contributions made to retirement plans can be included in your return all the way up until the due date. Are extensions included? You bet!

For those with an S corporation, you may qualify for a 20% deduction of qualified business income. However, you must include all your business income, all your earnings, and your spouse’s earnings and qualification may be affected by what you pay your employees.

If an owner is contemplating a C corporation conversion, it’s important to know that the company is taxed, as well as the owner’s dividends. So, in effect, it’s like double taxation.

Unfortunately, entertainment expenses, like event tickets and golfing, are no longer deductible, but 50% of food costs at these events is deductible.

So, whether you are comfortable with your tax bill or not, it may be beneficial to review it. Or better yet, find a trusted financial professional to help you navigate your options and make the best decisions for you and your family. After all, it’s all about optimization!

Live Life On Your Terms

Whether you want to travel more, do things you’ve always wanted to do, or just spend more time with the grandkids, we want to be your guide to help you get there.

Live Life On Your Terms

Whether you want to travel more, do things you’ve always wanted to do, or just spend more time with the grandkids, we want to be your guide to help you get there.