Better Investment Experience – Part Two

Resist Chasing Past Performance & Let Markets Work for You

March 2019

This is the second of a five-part series that will help you have a better investment experience. This isn’t a deep-dive into investing or the markets, but rather some basic concepts that investors often lose sight of.

Resist Chasing Past Performance

Some investors may resort to using track records as a guide to select funds in the present, reasoning that past success is likely to continue in the future. While that does make sense for some activities, does this assumption pay off with investing? Nope. The research offers strong evidence to the contrary.

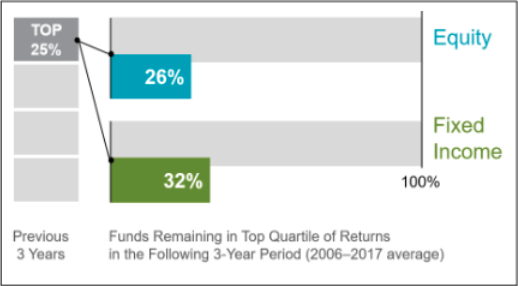

The exhibit below shows that among equity funds ranked in the top quartile (25%) based on previous three- year returns, only a small number of these remained in the top quartile three years later.

Growth Percentage of Top-Ranked Funds that Stayed on Top

Some investors select mutual funds based on their past returns. Yet, past performance offers little insight into a fund’s future returns. For example, most funds in the top quartile (25%) of previous three-year returns did not maintain a top-quartile ranking in the following three years.

A lack of persistence casts doubts on the ability of managers to consistently gain an informational advantage on the market. It goes without saying that some fund managers might be better than others, but track records alone may not provide enough insight to identify management skill. Stock and bond returns contain a lot of noise, and impressive track records may result from sheer luck. The assumption that strong past performance will continue often proves faulty, leaving many investors disappointed.

Let Markets Work for You

Most people look to the financial markets as their main investment avenue—and the good news is that the capital markets have rewarded long-term investors. The markets represent capitalism at work in the economy—and historically, free markets have provided a long-term return that has offset inflation.

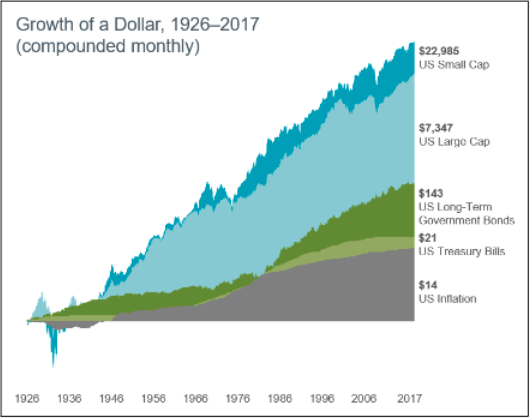

This is documented in the growth of wealth graph (below), which shows monthly performance of various indices and inflation since 1926. These indices represent different areas of the US financial markets, such as stocks and bonds. The data illustrates the beneficial role of stocks in creating real wealth over time. Treasury bills have barely covered inflation, while longer-term bonds have provided higher returns over inflation. US stock returns have far exceeded inflation and significantly outperformed bonds.

Growth of a Dollar, 1926–2017 (compounded monthly)

The financial markets have rewarded long- term investors. People expect a positive return on the capital they supply, and historically, the security and bond markets have provided the growth of wealth that has more than offset inflation.

Another key point is that not all stocks or bonds are the same. For example, consider the performance of US small cap stocks vs. US large cap stocks over this time period. A dollar invested in small cap stocks in 1926 would be worth considerably more today than a dollar invested in large cap stocks.

Keep in mind that there’s risk and uncertainty in the markets. Historical results may not be repeated in the future. Nevertheless, the market is constantly pricing securities to reflect a positive expected return going forward. Otherwise, people would not invest their capital.

A small cap or large cap generally refers to the value of the company. The “cap” here has to do with market capitalization and the value of the firm. A small cap firm is usually worth less than $2 billion and for a large cap, you’re looking a worth of more than $10 billion. Small caps offer more potential for growth and often, better returns.

The big take away with resisting using past performance as a future predictor and letting the markets work for you is that, once you invest in a solid model that aligns with your goals and risk comfort, then you can focus on other aspects of your life. Of course, you should reassess when you have a major change in your life, like a new baby or retirement, or at set intervals, such as annually or semi-annually. In other words, set up a good plan and let it work for you!

Monson Wealth Management Flat-Fee Program

Most Registered Investment Advisors charge a percentage of assets under management, which translates into the more money you have, the more you are charged, even though the servicing time may be the same as someone who has one-quarter of what you do.

Our Flat-Fee program is designed with these clients in mind. We don’t charge you more just because you have more.

Give us a call and in 15 minutes we can assess your situation to see if this makes sense for you.

“The MWM Flat-Fee Program is designed to give clients that have over $500k invested a fair shake.”

– Eldon Monson CFP®, RICP®

Live Life On Your Terms

Whether you want to travel more, do things you’ve always wanted to do, or just spend more time with the grandkids, we want to be your guide to help you get there.

Live Life On Your Terms

Whether you want to travel more, do things you’ve always wanted to do, or just spend more time with the grandkids, we want to be your guide to help you get there.